Short Introduction

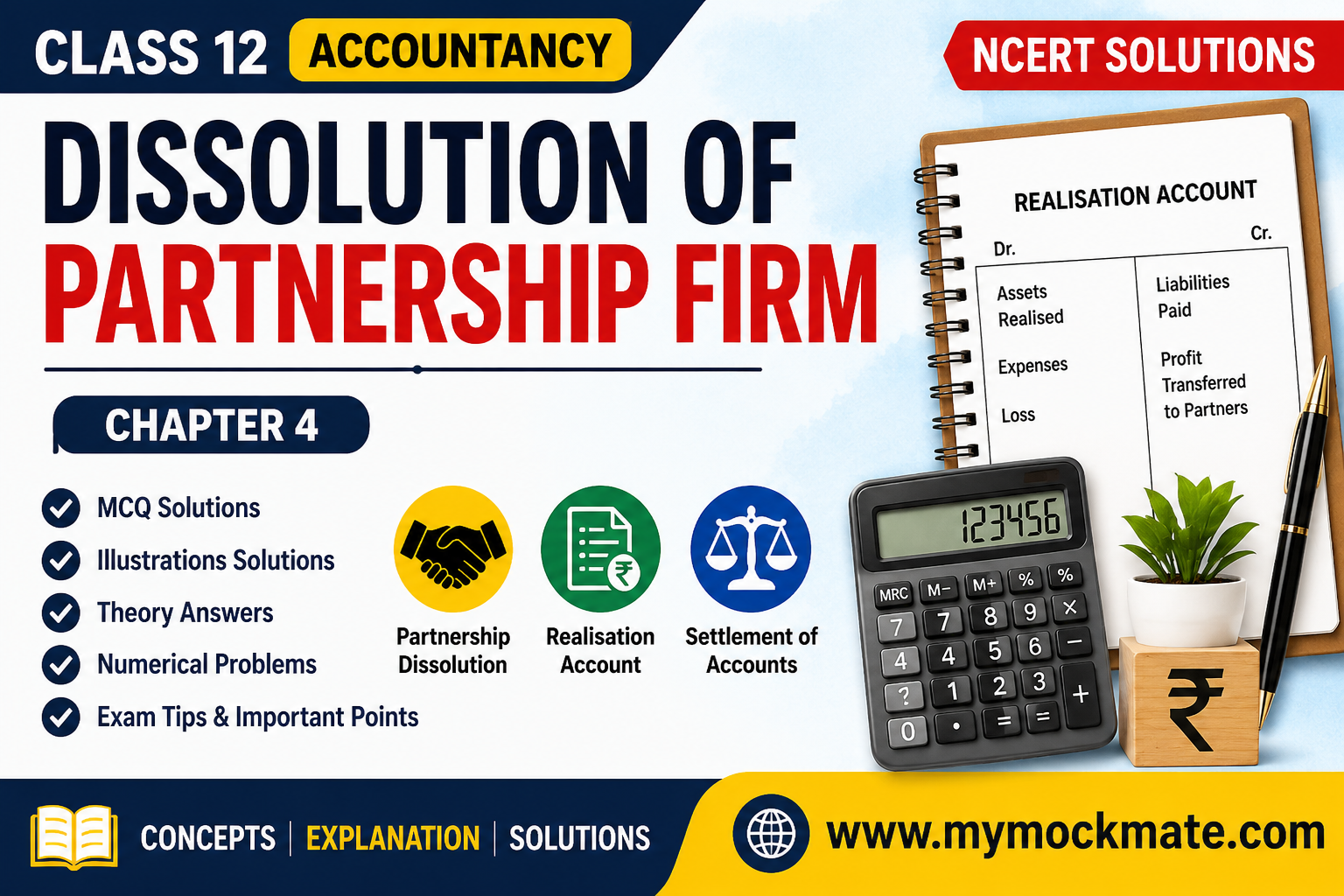

Dissolution of Partnership Firm refers to the complete closure of a partnership business. During dissolution, all assets are realized, liabilities are paid, and the remaining balance is distributed among partners according to their agreed profit-sharing ratio. This chapter explains the legal provisions, accounting treatment, and preparation of Realisation Account at the time of dissolution.

Quick Information Box

Chapter: Dissolution of Partnership Firm

Class: 12

Subject: Accountancy

Book: NCERT Accountancy Part-I

Topic Covered:

• Dissolution of Partnership

• Dissolution of Firm

• Realisation Account

• Settlement of Accounts

• Distribution of Assets and Liabilities

Concepts Used (Topics Covered)

• Meaning of Dissolution

• Difference between Dissolution of Partnership and Dissolution of Firm

• Modes of Dissolution

• Settlement of Claims

• Realisation Account

• Treatment of Assets and Liabilities

• Distribution of Profit and Loss on Realisation

Important Formulas

- Profit on Realisation

Profit on Realisation = Credit Side of Realisation Account − Debit Side of Realisation Account

- Loss on Realisation

Loss on Realisation = Debit Side of Realisation Account − Credit Side of Realisation Account

- Distribution of Realisation Profit/Loss

Partners’ Share = Profit or Loss × Profit Sharing Ratio

Question 1

Statement:

Dissolution of a partnership is different from dissolution of a firm.

Answer: True

Explanation:

Dissolution of partnership means change in relationship among partners due to admission, retirement or death. The business may continue.

Dissolution of a firm means complete closure of business and termination of partnership.

Question 2

Statement:

A partnership is dissolved when there is a death of a partner.

Answer: True

Explanation:

Death of a partner ends the existing partnership agreement and therefore dissolves the partnership relationship.

Question 3

Statement:

A firm is dissolved when all partners give consent to it.

Answer: True

Explanation:

A firm may be dissolved by agreement when all partners mutually agree to dissolve the firm.

Question 4

Statement:

A firm is compulsorily dissolved when a partner decides to retire.

Answer: False

Explanation:

Retirement causes dissolution of partnership but not necessarily dissolution of the firm.

Question 5

Statement:

Dissolution of a firm necessarily involves dissolution of partnership.

Answer: True

Explanation:

When a firm is dissolved, partnership automatically comes to an end.

Question 6

Statement:

A firm is compulsorily dissolved when all partners or all except one partner become insolvent.

Answer: True

Explanation:

Under the Partnership Act, the firm cannot continue if all partners or all except one become insolvent.

Question 7

Statement:

Court can order a firm to be dissolved when a partner becomes insane.

Answer: True

Explanation:

Permanent insanity of a partner is a valid ground for dissolution by court order.

Question 8

Statement:

Dissolution of partnership cannot take place without intervention of the court.

Answer: False

Explanation:

Partnership can be dissolved through mutual agreement without court intervention.

- Confusing dissolution of partnership with dissolution of firm.

- Treating retirement as compulsory dissolution.

- Ignoring legal provisions of Partnership Act, 1932.

- Assuming court intervention is always required.

• Learn all modes of dissolution.

• Remember the distinction table between partnership dissolution and firm dissolution.

• Revise provisions of Section 39 and Section 48.

• Frequently asked theory question in CBSE Board Exams.

- Which of the following leads to dissolution of partnership?

A. Admission of Partner

B. Retirement of Partner

C. Death of Partner

D. All of These

Answer: D

- Dissolution of firm means:

A. Change in ratio

B. Admission

C. Closure of business

D. Retirement

Answer: C

- Which Act governs partnership firms in India?

A. Companies Act

B. Partnership Act 1932

C. GST Act

D. Income Tax Act

Answer: B

- Which of the following is a ground for dissolution by court?

A. Insanity of Partner

B. Misconduct

C. Continuous Losses

D. All of These

Answer: D

- Dissolution of firm always results in:

A. Admission

B. Retirement

C. Dissolution of Partnership

D. None

Answer: C

Q1. What is dissolution of partnership?

Answer:

It refers to the termination of existing relationship among partners while business may continue.

Q2. What is dissolution of a firm?

Answer:

It refers to complete closure of business and termination of partnership relations.

Q3. Which section defines dissolution of firm?

Answer:

Section 39 of the Indian Partnership Act, 1932.

Q4. Is death of a partner dissolution of firm?

Answer:

Not necessarily. It dissolves partnership but the firm may continue.

Q5. Is court order compulsory for dissolution?

Answer:

No. Mutual agreement can also dissolve a firm.

Prepare Accountancy smarter with detailed NCERT solutions, chapter notes, MCQs, important formulas and board exam resources only on www.mymockmate.com.